The concept of a borderless life is no longer an exclusive luxury; for ultra-high-net-worth individuals (UHNWIs) and multinational families, it is an operational reality. Today’s global wealth networks are infinitely complex. The footprint of a particular family could consist of a matriarch living in London, offspring running a technology startup in California, factories in Singapore, and investments in real estate all around the Mediterranean region.

However, while working on a multinational scale presents great opportunities, it also creates enormous friction. Global wealth networks constantly bump up against conflicting tax codes, fragmented legal jurisdictions, political instability, and aggressive regulatory oversight.

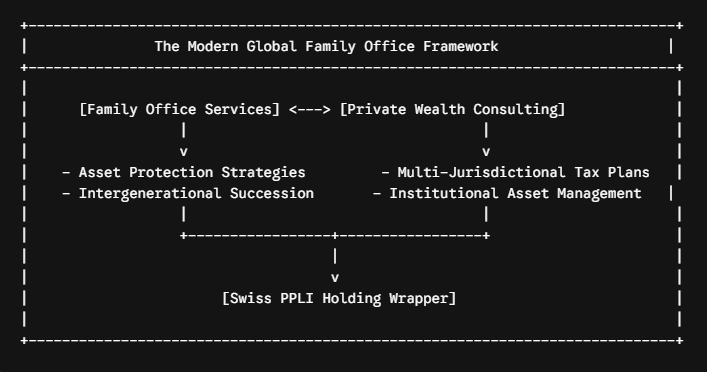

To survive and thrive, traditional asset management is no longer enough. Forward-thinking families are looking beyond standard private wealth consulting to holistic frameworks that bridge the gap between private wealth advisory and institutional corporate engineering. At the absolute center of this paradigm shift is the strategic deployment of Swiss Private Life Insurance.

Evolution of Global Wealth Networks

In the past, dealing with significant wealth had always been rather local. The family had created the business, worked with a local private wealth adviser, used conventional wealth management solutions, and even insured their business operations locally. Succession planning included making a simple will or forming a local trust.

But the fast swiftness of globalization in the 21st century shattered these silos. Money has become portable, decentralized, and highly interlinked.

As global wealth networks evolved, family office services had to pivot from simple administrative management to complex cross-border orchestration. The challenges multiplying for these networks include:

- Overlapping Tax Jurisdictions: Being taxed on worldwide income across multiple countries simultaneously.

- Information Exchange Regimes: Navigating the automated compliance demands of the CRS and FATCA.

- Asset Fragmentation: Managing disparate portfolios consisting of liquid equities, real estate, private equity, and digital investments scattered globally.

Because traditional trusts and standalone holding companies are increasingly challenged by foreign tax authorities, global wealth networks have spent the last decade searching for a vehicle that offers universal compliance, robust protection, and absolute operational flexibility.

The Strategic Role of Swiss PPLI

This is where Swiss Private Placement Life Insurance enters the conversation—not merely as an insurance product, but as an elite asset-holding architecture.

At its core, PPLI is a specialized, variable life insurance policy engineered specifically for affluent investors. Instead of purchasing a retail policy with fixed, pre-selected investments, the policyholder wraps their own highly customized, diverse asset portfolio within the life insurance contract.

But why has Switzerland become the definitive hub for this specific structure?

The services that Switzerland provides for its wealth management industry have endured through centuries of international turmoil due to two skills: solid asset protection and effective coordination across several disciplines. In cases where a global network is relying on Swiss PPLI, they are not only purchasing a policy but rather entering an exclusive system of private wealth consultancy, elite banking, and commercial insurance.

Under Swiss law, the assets placed inside a PPLI policy are legally segregated from the balance sheet of the insurance provider. This means if the insurer or the custodian bank faces financial distress, the policyholder’s assets are entirely immune to third-party creditor claims. It is an unshakeable fortress built on Swiss regulatory stability.

Cross-Jurisdictional Wealth Management

The most serious headache in dealing with a family office on an international level would be that of tax friction among jurisdictions. The minute any individual earns dividends, makes capital gains or sells off a company, he is immediately subjected to serious taxes.

The Swiss PPLI wrapper elegantly solves this via the principle of tax deferral and legal transformation.

The Legal Shift: When assets are placed into a Swiss PPLI policy, the insurance company becomes the legal owner of those underlying investments. The ultimate investor owns the policy, not the assets themselves.

Since the insurer technically owns the asset, the asset in the underlying portfolio is allowed to be traded, rebalanced, dividend reinvested, and liquidated without generating an immediate tax burden on the income or gains for the investor. Money will grow in a tax-protected manner, much better than any taxable investment portfolio.

In addition, life insurance is a globally accepted legal principle. Whereas a trust created in a common law jurisdiction, such as the United States and United Kingdom, would be seen with utter suspicion or not be recognized at all in civil law jurisdictions like France, Germany, and Italy, the life insurance would certainly be understood in all jurisdictions. This makes Swiss PPLI the ultimate passport for cross-border wealth optimization.

Risk Diversification Through Global Structures

Diversification of risk means much more than merely combining equities, fixed income, and real estate investments. It also means diversifying the legal ownership of these investments. The global wealth network utilizes Swiss PPLI as a master shield against systemic regional risks.

Consider a multi-generational family with operating companies located in emerging or politically volatile markets. They require comprehensive commercial insurance services and localized insurance coverage for businesses to protect their day-to-day physical operations. However, leaving the surplus capital generated by those businesses in the same volatile jurisdiction is a massive risk.

By funneling corporate distributions out of volatile regions and wrapping them into a Swiss PPLI structure, the family achieves ultimate risk isolation:

- Geopolitical Shielding: The family’s main wealth holdings are legally secured within the country of Switzerland, free from any local political turmoil, expropriation, or currency depreciation.

- Lawsuit Shielding: Because the money is included in the Swiss insurance contract, it will be protected against any lawsuits or divorces that the heirs face elsewhere.

Enhancing Liquidity and Flexibility

A frequent fallacy associated with robust wealth structuring is that ironclad asset protection is achieved only by sacrificing liquidity and control. Swiss PPLI provides a clear refutation of this fallacy.

The policyholder has no option but to hand over discretionary trading of the underlying assets to a professional asset manager, yet the structure is highly liquid.

Flexibility Features of Swiss PPLI

– Custom Asset Inclusion (Private Equity, Real Estate, Fine Art)

– Tax-Free Policy Loans for Immediate Liquidity

– Smooth, Probate-Free Intergenerational Wealth Transfer

Global wealth networks make ample use of such a feature. If any member of the family needs cash for some business or real estate purpose urgently, there is no need to break down the network or sell any assets for taxable purposes. Instead, they can simply take a tax-efficient loan against the cash value of the PPLI policy.

Additionally, the flexibility extends to succession. When the patriarch or matriarch passes away, the entire global portfolio held within the PPLI wrapper bypasses the agonizingly slow, public, and expensive probate courts. The policy proceeds are paid directly, privately, and swiftly to the designated global beneficiaries—often entirely free of inheritance tax.

Conclusion: Borderless Wealth Strategies

As the world continues to erect complex legal and regulatory boundaries, global wealth networks must adopt strategies that effortlessly scale past them. Relying on fragmented, regional financial plans is an invitation to administrative chaos and financial inefficiency.

The integration of Swiss PPLI into a modern family office framework represents the pinnacle of borderless wealth management. It transforms a scattered, highly vulnerable global portfolio into a unified, compliant, and deeply protected financial fortress. Through the unique combination of the eternal security of the Swiss private banking model with the complex layer of international insurance structuring, it is now possible for global business networks to have their money flow as freely as they do.